With higher education costs rising sharply in India and overseas, choosing the right education loan can save students and families lakhs of rupees over the repayment period.

The cost of higher education continues to climb across India and major international study destinations, making education loans an increasingly important financing option for students.

Whether you are planning to pursue an undergraduate degree in India, a master’s program abroad, or a professional course, the interest rate on your education loan can significantly impact your long-term financial health.

A difference of just 1% to 2% in interest rates may seem small initially, but over a repayment tenure of 10 to 15 years, it can translate into substantial savings.

That is why comparing education loan interest rates in June 2026 across public and private sector banks is essential before submitting an application.

However, borrowers should remember that interest rates are only one part of the equation. Processing fees, moratorium periods, collateral requirements, repayment flexibility, and prepayment charges also influence the overall cost of borrowing.

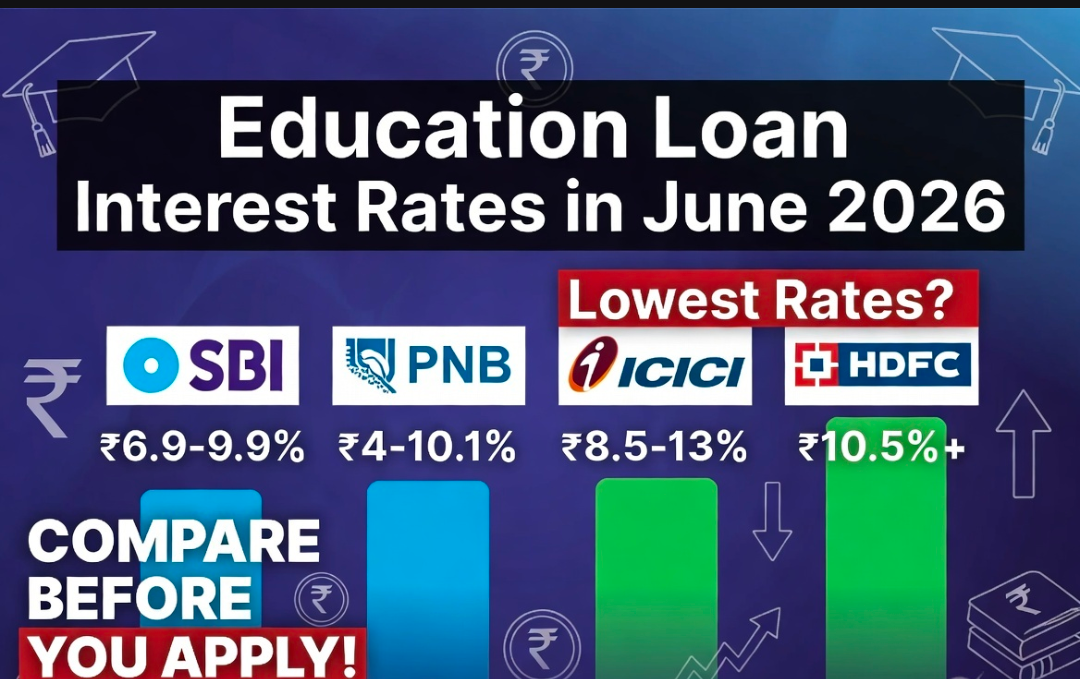

Education Loan Interest Rates: June 2026 Comparison

The following rates are indicative for education loans above ₹7.5 lakh for overseas studies and may vary based on the applicant’s academic profile, institution, co-applicant income, credit score, and loan tenure.

| Public Sector Bank | Indicative Interest Rate |

|---|---|

| Punjab National Bank | 8.10% |

| State Bank of India | 8.90% |

| Canara Bank | 9.25% |

| Union Bank of India | 9.25% |

| Bank of Baroda | 10.25% |

| Private Sector Bank | Indicative Interest Rate |

|---|---|

| ICICI Bank | 9.00% |

| IDFC FIRST Bank | 9.50% |

| IDBI Bank | 9.90% |

| Axis Bank | 10.81% |

| HDFC Bank | 12.50% |

Among the banks listed, Punjab National Bank currently offers the lowest indicative interest rate, while HDFC Bank has the highest rate for comparable overseas education loans.

Public Sector vs Private Sector Banks: Which Is Better?

Public sector banks typically offer lower interest rates and longer repayment tenures, making them an attractive choice for cost-conscious borrowers.

However, loan processing timelines can be longer, and documentation requirements may be more extensive.

Private sector banks, on the other hand, often provide faster approvals, digital application processes, and greater flexibility for students admitted to premium institutions.

These advantages may come at the cost of higher interest rates and additional fees.

| Factor | Public Sector Banks | Private Sector Banks |

|---|---|---|

| Interest Rates | Generally lower | Usually higher |

| Loan Processing Speed | Moderate | Faster |

| Digital Experience | Basic to moderate | Advanced |

| Documentation | More extensive | Relatively streamlined |

| Repayment Flexibility | Moderate | Higher |

What Determines Your Education Loan Interest Rate?

The advertised rate is rarely the final rate offered to every applicant.

Banks assess multiple factors before determining the applicable interest rate.

- Academic profile: Admission to reputed institutions can improve loan terms.

- Course type: Professional courses with strong placement records may attract lower rates.

- Co-applicant’s income: A financially stable co-borrower can strengthen eligibility.

- Credit score: The credit history of the co-applicant significantly affects pricing.

- Collateral: Secured loans often carry lower interest rates than unsecured loans.

- Loan amount and tenure: Larger loan amounts and longer tenures may impact pricing.

Understanding the Moratorium Period

One of the most important features of an education loan is the moratorium period.

This is the duration during which students are not required to begin full EMI payments.

Typically, the moratorium includes the course duration plus an additional six to twelve months after graduation, allowing students time to secure employment.

However, borrowers should check whether interest accrues during this period and whether simple or compound interest applies.

Paying interest during the moratorium, if financially feasible, can significantly reduce the total repayment burden.

Hidden Costs Borrowers Often Ignore

Many students focus solely on interest rates while overlooking other charges that can increase borrowing costs.

- Processing fees

- Documentation charges

- Insurance premiums

- Legal and valuation fees for collateral-backed loans

- Currency conversion charges for overseas disbursements

- Late payment penalties

- Prepayment or foreclosure charges

Always request a detailed schedule of charges before signing the loan agreement.

How to Reduce Your Education Loan Burden

Strategic planning can help borrowers save a substantial amount over the life of the loan.

- Compare offers from multiple lenders before applying.

- Maintain a strong credit profile for the co-applicant.

- Choose a shorter tenure if affordable.

- Pay interest during the moratorium period.

- Use scholarships and grants to reduce the loan amount.

- Make partial prepayments whenever possible.

- Consider refinancing if interest rates decline in the future.

Should You Opt for a Secured or Unsecured Education Loan?

Secured education loans require collateral such as property, fixed deposits, or other assets.

These loans generally offer lower interest rates and higher borrowing limits.

Unsecured loans do not require collateral but typically carry higher interest rates and stricter eligibility criteria.

Students pursuing expensive international programs should carefully evaluate the risks and benefits before pledging family assets.

Why Repayment Planning Matters More Than Loan Approval

Securing an education loan is only the first step.

The real challenge begins after graduation.

Before borrowing, students should realistically assess expected starting salaries, employment opportunities in their chosen field, and monthly repayment obligations.

Financial experts generally recommend keeping total EMI commitments within a manageable percentage of monthly income to avoid future financial stress.

Borrowers should also create an emergency fund to prevent missed payments during periods of unemployment or career transitions.

Conclusion

Education loans can open doors to life-changing opportunities, but choosing the wrong lender can significantly increase the cost of higher education.

While Punjab National Bank, State Bank of India, and ICICI Bank currently offer some of the most competitive education loan rates in June 2026, the lowest interest rate should not be the only deciding factor.

Students and families must evaluate processing fees, repayment flexibility, moratorium terms, collateral requirements, and future earning potential before making a decision.

A well-planned education loan is not just a financing tool—it is an investment in your future. Taking the time to compare options carefully today can lead to substantial savings and greater financial stability tomorrow.

For breaking news and live news updates, like us on Facebook or follow us on Twitter and Instagram. Read more on Latest Careers on thefoxdaily.com.

COMMENTS 0