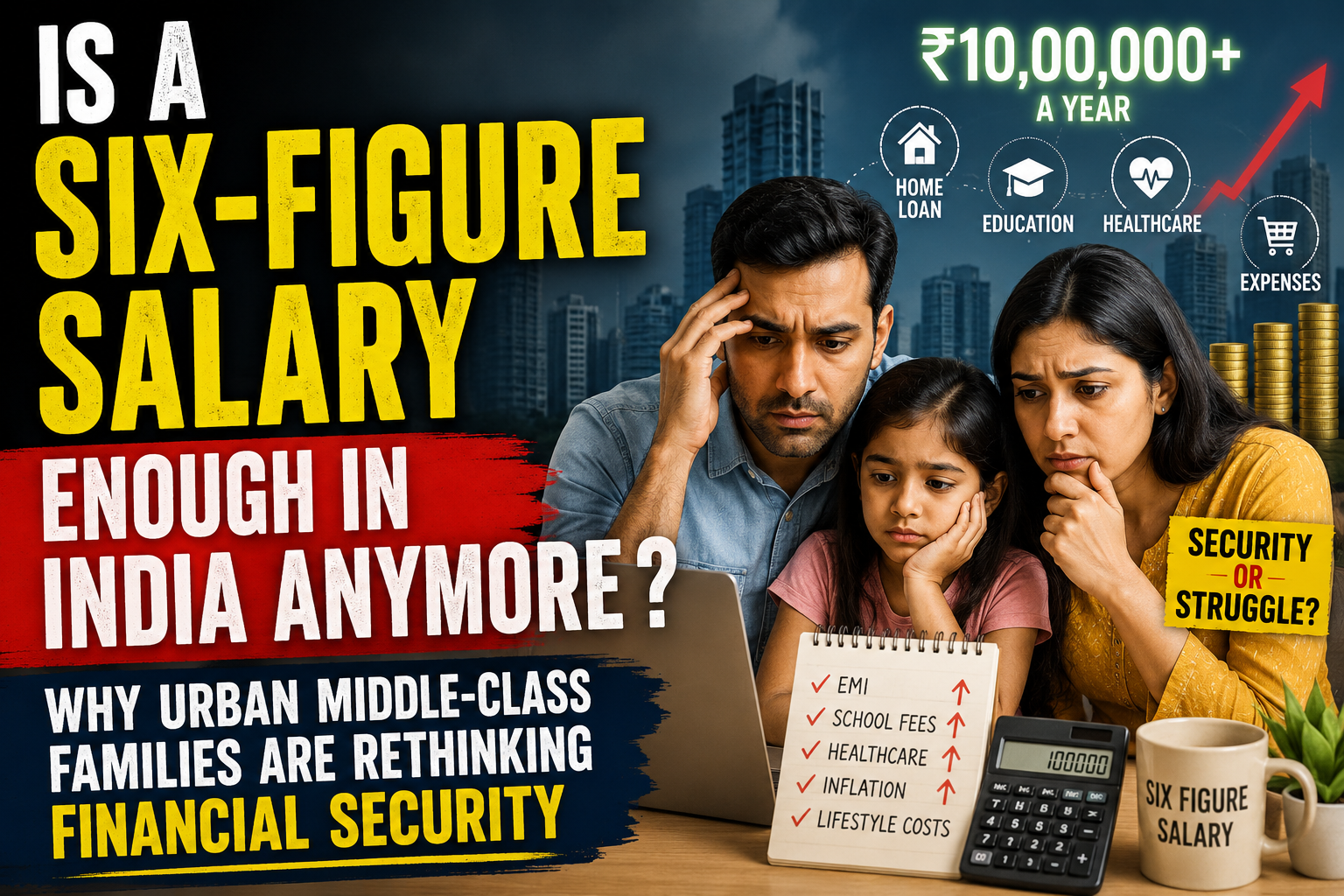

For years, earning a six-figure monthly salary was considered a defining milestone for India’s middle class. Crossing the Rs 1 lakh-per-month mark signified career success, financial stability, and the promise of a comfortable life.

Today, that equation is being challenged.

Across major cities such as Bengaluru, Mumbai, Delhi-NCR, Hyderabad, and Pune, a growing number of professionals are discovering that a salary once associated with prosperity no longer guarantees financial peace of mind.

The conversation gained momentum after reports emerged of a Bengaluru technology professional taking up taxi driving as a side hustle despite earning a respectable income. The story resonated widely because it reflected a reality many urban Indians already understand: higher earnings do not automatically translate into financial security.

The question is no longer whether Rs 1 lakh a month is a good salary. Instead, it is whether that income can keep pace with rapidly rising costs, evolving lifestyle expectations, and long-term financial goals.

What Does a Six-Figure Salary Mean in India Today?

A six-figure monthly income—typically defined as earning Rs 1 lakh or more per month—still places individuals among the country’s higher earners.

However, income alone offers an incomplete picture of financial well-being.

The value of a salary depends heavily on factors such as location, family size, debt obligations, lifestyle choices, and future goals.

A single professional earning Rs 1 lakh per month in a tier-2 city may enjoy significant financial flexibility. A family of four living in Mumbai or Bengaluru with home loan payments, school fees, and ageing parents to support may experience an entirely different reality.

Financial comfort has become increasingly relative.

| Factor | Impact on Financial Comfort |

|---|---|

| City of Residence | Higher rents and living costs reduce disposable income |

| Housing Expenses | EMIs and rent often consume a large share of income |

| Family Size | More dependents increase monthly expenses |

| Education Costs | Private schooling significantly affects savings capacity |

| Healthcare and Insurance | Premiums continue to rise annually |

| Lifestyle Choices | Travel, dining, and subscriptions increase spending |

The Rising Cost of Urban Living

India’s major urban centres have undergone significant economic transformation over the past decade.

While salaries in sectors such as technology, finance, consulting, and healthcare have increased, living costs have risen at an equally rapid pace.

Housing remains the largest expense for most urban households.

Property prices and rental costs have surged across major metropolitan areas, forcing many professionals to allocate a substantial portion of their income toward accommodation.

Beyond housing, everyday expenses have also increased.

- Private school fees continue to rise annually.

- Healthcare costs and insurance premiums have increased.

- Transportation expenses have grown due to fuel prices and commuting needs.

- Utility bills, subscriptions, and digital services now form a regular part of household budgets.

- Higher interest rates have increased the burden of loan repayments.

For many families, salary increments often feel temporary because additional income is quickly absorbed by rising expenses.

The Hidden Impact of Lifestyle Inflation

One of the most significant yet overlooked challenges facing India’s middle class is lifestyle inflation.

As incomes increase, spending habits often evolve alongside them.

What was once considered a luxury gradually becomes a necessity.

Frequent dining out, premium gadgets, international vacations, private schooling, larger homes, and subscription-based services have become increasingly common among urban households.

While these choices can improve quality of life, they also create higher fixed expenses that are difficult to reduce during periods of financial uncertainty.

In many cases, professionals are not struggling because they earn too little—they are struggling because their expenses have expanded at the same pace as their incomes.

Why More Professionals Are Turning to Side Hustles

The rise of side hustles reflects a changing attitude toward financial security.

Increasingly, salaried professionals are diversifying their income sources through freelance work, consulting, content creation, online teaching, investing, and small businesses.

This shift is driven by two key factors.

First, additional income provides a buffer against rising living costs and unexpected expenses.

Second, professionals recognize that relying on a single source of income carries risks in an uncertain economic environment.

Side hustles are no longer viewed as signs of financial distress. Instead, they are becoming an essential component of modern wealth-building strategies.

| Traditional Approach | Modern Approach |

|---|---|

| Single salary source | Multiple income streams |

| Employer-funded retirement security | Self-managed investments |

| Fixed career path | Flexible income opportunities |

| Long-term job stability | Continuous skill development |

The Social Media Effect on Financial Expectations

Financial pressure is not driven solely by rising costs.

Social media has fundamentally changed how people define success.

Platforms filled with images of luxury homes, premium lifestyles, expensive cars, and international travel have created new benchmarks for achievement.

As a result, many individuals compare their financial progress with curated versions of other people’s lives.

This constant exposure can blur the distinction between needs and wants.

What was once aspirational now appears ordinary, creating a sense that one’s current income is never quite enough.

Psychologists often refer to this phenomenon as the “comparison trap”—the tendency to measure personal success against unrealistic standards.

Even high earners can experience financial dissatisfaction when expectations continue to rise faster than income.

Why Financial Anxiety Feels More Intense Today

Modern middle-class households face a unique combination of responsibilities.

Many professionals are simultaneously managing multiple long-term goals, including:

- Buying a home.

- Funding children’s education.

- Supporting ageing parents.

- Building retirement savings.

- Maintaining emergency funds.

- Protecting against medical emergencies.

This creates a financial paradox.

Today’s professionals often earn significantly more than previous generations did at the same age. Yet they frequently report feeling less financially secure.

The reason lies in the complexity of modern financial life.

Earlier generations benefited from lower housing costs, simpler lifestyles, and stronger informal support systems. Today’s urban professionals must navigate higher expenses and greater financial uncertainty.

How Much Money Is Actually Enough?

There is no universal answer to this question.

Financial security is deeply personal and depends on individual circumstances.

Instead of focusing exclusively on income, experts increasingly recommend evaluating financial health using broader indicators.

| Financial Indicator | Target Goal |

|---|---|

| Emergency Fund | Six to twelve months of expenses |

| Savings Rate | At least 20% of monthly income |

| Debt-to-Income Ratio | Below 35% |

| Retirement Contributions | Consistent long-term investing |

| Insurance Coverage | Adequate health and life protection |

Ultimately, financial freedom is less about earning a specific amount and more about aligning spending with priorities while maintaining resilience against unexpected events.

The New Definition of Middle-Class Success

For decades, the middle-class dream followed a predictable formula: secure a stable job, buy a home, educate children, and retire comfortably.

Those goals remain relevant, but achieving them has become more expensive and complicated.

Today’s definition of success increasingly includes financial flexibility, diversified income sources, manageable debt, and the ability to make choices without constant financial stress.

In other words, wealth is no longer measured solely by income. It is measured by control over time, money, and future opportunities.

What Urban Professionals Can Do to Stay Financially Secure

- Create a detailed monthly budget and track expenses regularly.

- Avoid increasing lifestyle costs immediately after salary hikes.

- Build multiple income streams where possible.

- Prioritise emergency savings before discretionary spending.

- Invest consistently for long-term goals.

- Review insurance coverage annually.

- Focus on skill development to maintain earning potential.

- Set realistic financial expectations based on personal priorities rather than social comparisons.

Conclusion

A six-figure salary in India remains a significant achievement, but it no longer guarantees the level of comfort it once did.

Rising living costs, housing expenses, changing aspirations, and evolving financial responsibilities have transformed the economics of middle-class life.

The challenge facing urban professionals is not simply earning more money—it is managing money more effectively.

As India’s economy continues to grow, financial security will increasingly depend on disciplined spending, long-term planning, diversified income, and realistic expectations.

In today’s urban India, a good salary may still open doors, but lasting peace of mind comes from building financial resilience—not just increasing income.

For breaking news and live news updates, like us on Facebook or follow us on Twitter and Instagram. Read more on Latest Careers on thefoxdaily.com.

COMMENTS 0