Every few days, another Social Media post claims that a modest monthly SIP can turn an ordinary investor into a millionaire. The formula usually sounds irresistible: invest Rs 5,000 per month, stay invested for 10 years, ignore market noise, and become wealthy.

While SIPs are undoubtedly one of the most powerful wealth-building tools available to retail investors, the reality is more nuanced than many advertisements suggest. A 10-year SIP does not automatically make anyone rich. What it does is dramatically improve the odds of wealth creation by harnessing some of the most powerful forces in economics, mathematics, and human behavior.

To truly understand whether a 10-year SIP can make you rich, we need to look beyond marketing slogans and examine how compounding works, why market crashes can be beneficial, what History teaches about investing, and why investor psychology often matters more than Stock Market returns.

What Is a SIP and Why Has It Become So Popular?

A Systematic Investment Plan (SIP) allows investors to invest a fixed amount into a mutual fund at regular intervals, usually monthly. Rather than trying to predict market highs and lows, investors buy units consistently regardless of market conditions.

The popularity of SIPs has exploded because they solve one of investing’s biggest challenges: discipline.

- They encourage regular investing.

- They remove the need to time the market.

- They automate wealth creation.

- They make equity investing accessible.

- They leverage long-term compounding.

For many investors, SIPs transform investing from a complicated activity into a habit.

The Biggest Myth: A 10-Year SIP Does Not Guarantee Wealth

The first misconception that needs to be addressed is the belief that investing through SIPs for 10 years guarantees profits.

Financial Markets do not offer guarantees.

Equity Mutual Funds are market-linked investments. Their returns depend on economic growth, corporate earnings, global events, interest rates, Inflation, and investor sentiment.

A decade significantly improves the probability of earning positive returns, but it does not eliminate risk.

Markets can experience prolonged periods of underperformance. Certain funds may struggle due to poor management decisions. Economic disruptions can affect returns for years.

The truth is simple: time improves the odds, but it does not guarantee the outcome.

The Mathematics Behind Why SIPs Work

At its core, SIP investing is not about finance. It is about mathematics.

The real engine behind SIP success is the interaction between compounding and time.

Compounding occurs when investment returns begin generating their own returns. Instead of earning gains only on your original investment, you start earning gains on previous gains.

This creates exponential growth rather than linear growth.

Consider two investors:

- Investor A invests Rs 5,000 monthly for 10 years.

- Investor B waits five years and then invests Rs 10,000 monthly for the next five years.

Both invest the same overall amount. Yet Investor A often ends up with a larger corpus because the earlier investments have more time to compound.

The lesson is powerful: in investing, time is often more important than the amount invested.

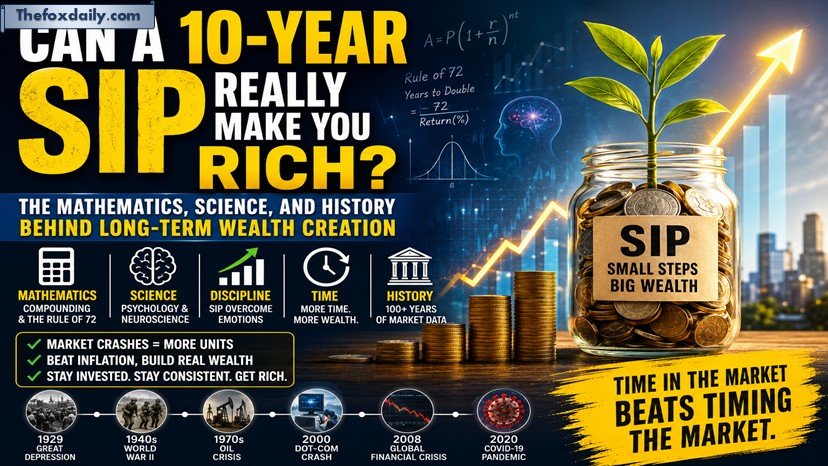

The Rule of 72: The Simplest Wealth Formula

One of the most useful concepts for SIP investors is the Rule of 72.

The formula estimates how long money takes to double:

\text{Years to Double} = \frac{72}{\text{Annual Return (%)}}

| Annual Return | Approximate Doubling Time |

|---|---|

| 6% | 12 Years |

| 8% | 9 Years |

| 10% | 7.2 Years |

| 12% | 6 Years |

| 15% | 4.8 Years |

This explains why long-term investors become obsessed with consistency rather than short-term performance. Every additional year allows compounding to accelerate.

Why Market Crashes Can Actually Help SIP Investors

This is perhaps the most misunderstood aspect of investing.

Most investors fear market crashes. Experienced SIP investors often view them as opportunities.

When markets decline, SIPs continue purchasing mutual fund units at lower prices. This means investors accumulate more units with the same monthly investment.

When markets eventually recover, those extra units contribute significantly to wealth creation.

Ironically, the periods investors fear the most often become the periods that generate the highest long-term rewards.

The problem is not volatility. The problem is panic.

Many investors stop SIPs or redeem investments during corrections, destroying the very advantage SIPs are designed to create.

The Science of Investor Psychology

One of the biggest discoveries in modern finance is that investor behavior often matters more than market returns.

Behavioral economists have spent decades studying why people make poor financial decisions.

One of their most important findings is a concept called loss aversion.

research suggests that people feel the pain of losses roughly twice as strongly as the pleasure of gains.

This explains why investors panic during market downturns.

Even when they understand that markets recover over time, emotions often override logic.

The result is predictable:

- Investors buy during euphoric bull markets.

- Investors sell during fearful bear markets.

- Investors chase recent winners.

- Investors abandon long-term plans.

SIPs help solve this problem by automating investment decisions and reducing emotional interference.

What Neuroscience Reveals About Investing

Brain imaging studies have shown that financial losses activate regions of the brain associated with fear and physical pain.

In other words, market declines do not merely feel uncomfortable they can trigger biological stress responses.

This explains why staying invested during market crashes feels so difficult.

SIPs work partly because they remove decision-making from moments of emotional stress.

Rather than relying on willpower, investors rely on systems.

In this sense, SIPs are not just financial tools. They are behavioral tools designed to overcome human psychological weaknesses.

What 100 Years of Market History Teach Us

History offers one of the strongest arguments for long-term investing.

Over the past century, financial markets have survived:

- The Great Depression

- World War II

- The Oil crisis

- The Dot-Com Crash

- The Global Financial Crisis

- The Covid-19 Pandemic

- Numerous geopolitical conflicts

Every crisis felt unprecedented at the time.

Every crisis triggered predictions of permanent decline.

Yet markets eventually recovered because economies continued producing goods, services, innovation, and productivity growth.

The lesson is not that markets never fall.

The lesson is that long-term economic progress has historically been stronger than short-term disruptions.

The Hidden Enemy: Inflation

Most investors focus on market crashes. However, inflation may be a much bigger threat.

A market correction can temporarily reduce portfolio value.

Inflation reduces purchasing power every year.

For example, if inflation averages 6% annually, a product costing Rs 100 today could cost nearly Rs 180 in about ten years.

Money sitting idle gradually loses value.

This is why investing is not simply about generating returns. It is about growing wealth faster than inflation.

Real wealth is measured by purchasing power, not portfolio size.

Can a Rs 5,000 SIP Really Make You Rich?

The answer depends on what “rich” means.

A Rs 5,000 monthly SIP can create meaningful wealth over time, especially if investments grow at reasonable long-term rates.

However, becoming financially wealthy usually requires more than simply maintaining the same SIP forever.

Factors that influence outcomes include:

- Investment duration

- Rate of return

- Fund quality

- Inflation

- Contribution increases

- Investor discipline

The investors who build substantial wealth are typically those who increase their SIP contributions as their income grows.

The Most Powerful Strategy Most Investors Ignore

One of the biggest mistakes investors make is keeping SIP contributions fixed for years.

As salaries increase, investments should ideally increase as well.

This approach, known as a step-up SIP, can dramatically improve wealth creation.

For example, increasing SIP contributions by just 10% annually can create a significantly larger corpus compared to maintaining a fixed contribution.

The real secret of wealth creation is not merely staying invested it is investing progressively larger amounts over time.

The Evolutionary Reason Investing Feels Difficult

Human beings evolved to prioritize immediate survival over future rewards.

This instinct helped our ancestors survive dangerous environments.

Unfortunately, it works against successful investing.

Financial markets reward patience, while human instincts encourage immediate action.

SIPs effectively counter this evolutionary bias by creating a structure that rewards consistency over reaction.

This is one reason why many successful investors believe wealth creation is more about behavior management than stock selection.

The Final Truth About 10-Year SIPs

After examining the mathematics, science, psychology, economics, and history behind investing, the answer becomes clear.

A 10-year SIP is not a guaranteed path to riches.

What it does provide is something far more valuable: a proven framework for long-term wealth creation.

It harnesses the power of compounding, benefits from market volatility through rupee cost averaging, overcomes psychological biases, and aligns with historical patterns of economic growth.

However, success still depends on discipline, patience, fund selection, inflation awareness, and the willingness to remain invested during difficult periods.

The investors who become wealthy through SIPs are rarely the smartest market timers.

They are usually the most consistent.

They continue investing when others panic.

They increase contributions as income grows.

They focus on decades rather than months.

Most importantly, they understand that wealth creation is not an event it is a process.

So, can a 10-year SIP make you rich?

Yes, it can dramatically improve your chances.

But the real magic is not in the SIP itself.

The magic is in staying invested long enough for mathematics, human progress, and compounding to work in your favor.

For breaking news and live news updates, like us on Facebook or follow us on Twitter and Instagram. Read more on Latest Personal Finance on thefoxdaily.com.

COMMENTS 0